Means and Instruments of Payment in International Trade / Medios e Instrumentos de Pago En el Comercio Internacional

English Version

Means and Instruments of Payment in International Trade

Introduction

For the proper development of all operations related to foreign trade, it is a fundamental factor to determine and clarify what is related to the payment of the goods or services acquired, since in most cases when we enter the import and export processes this translates into large sums of money that are at stake.

In these commercial processes there are basically three fundamental actors, firstly there is the importer, which is nothing more than the natural or legal person who makes the purchase and therefore is responsible for making the corresponding payment, secondly we have the exporter, who can also be a natural or legal person, but this time he is in charge of carrying out the dispatch of the good or service that is being traded and therefore the latter becomes the beneficiary of the respective payment and therefore Finally, there is the bank, which will always serve as a connection factor between the importer, this entity usually has different roles depending on the financial transaction process, that is, in some cases it can be a simple mediator while in others it is an indisputable guarantor. payment.

In the present investigation of a descriptive nature, reference is made to the various means of payment that exist within foreign trade, therefore a respective conceptualization of each one of them is carried out and it is preceded by classifying them according to their characteristics, with which it is sought achieve a better understanding of them and be able to determine in what circumstances they are used, in addition to this classification, various assessments are also made, ranging from the trust existing between the parties to the security factors that are decisive for the completion of the purchase.

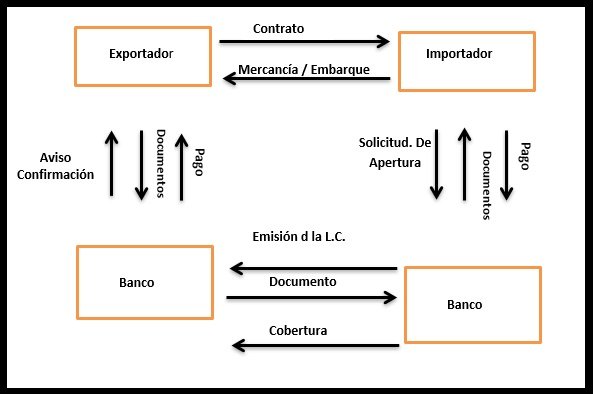

By way of simplification and to achieve a better understanding of the work carried out as the final point of this research, a scheme is presented that breaks down in a didactic and simple way all the means of payment and their existing classifications within international trade as we know it in the present.

To carry out a commercial operation at the export and import level, it is important to know the various means of payment existing in international trade, since it is through financial instruments through which the monetary cancellation corresponding to the cost of the goods and services can be made. services that are traded, it is important to highlight that these instruments have high standards of security and transparency, in addition, their versatility allows them to be adopted to the circumstances of each commercial operation.

Factors that will determine the choice in the means of payment

Just as it happens in any commercial operation when we talk about payments in the export and import processes, it is important to highlight that the choice of cancellation instrument will depend on various factors that will be determined between the buyer and the seller. In international trade there is no manual or rule that determines exactly which instrument should be used, therefore this is considered a matter that is resolved directly in the direct negotiation processes that occur between the parties involved on a daily basis. which in a general and most common way it can be determined that the determining factors in most cases are the following:

A) Degree of trust existing between the parties: This factor is decisive in the commercial relationship, since when there is greater trust, more flexible or open means of payment could be chosen, through which the financial operation would be faster.

B) Costs: The price of the traded merchandise will also determine the best form of payment for it.

C) Size of the Parties: The economic capacity of both the buyer and the seller will determine the forms of payment that can be cash or through bank credits.

D) Country Risk: Some authors include country risk among the determining factors in the choice of means of payment, since when we talk about a State that is in turmoil or immersed in unfavorable economic circumstances it will not be the most advisable accept payments from bank credits or similar methods, but on the contrary, the methods that are direct and in cash are preferred in order to avoid possible insolvency.

Through this description, it can be seen that the factors involved in the choice of payment method are highly variable and depend exclusively on the relationship between buyer and seller, which makes it possible to make procedures more flexible and adjust to the specific needs of the parties involved in the transaction. operation, in addition to guaranteeing security and reliability in payments.

Means of Payment in International Trade

Means or instruments of international payment are those mechanisms or operational modalities through which the importer can cancel the contract or commitment to pay with the exporter as a result of the purchase or contracting of a commercial good or service, which in the Most of the cases will be described in a legal document called an International Purchase-Sale Agreement. Within the means of payment we can highlight the following:

1-Checks

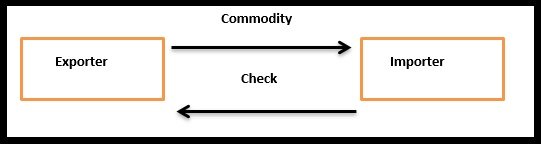

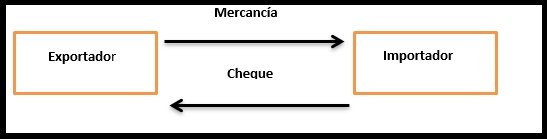

A check is an accounting document through which a person is authorized to extract or collect a certain amount of money from an account, which is deposited in a bank without the presence of the account holder. Checks are usually one of the safest methods for the cancellation of goods and services abroad, since it is perfectly verifiable as far as the funds are concerned, they also represent a legal document which can be used as evidence in case of a payment default.

Checks at the international level have a similar structure, through which a greater understanding and greater security are sought. The data that these payment mechanisms must contain are the following: 1) Date of Issue. 2) Amount in letters and numbers. 3) Place of Payment (where the account is located) 4) Name of the Beneficiary 5) Number and name of the drawer's account. 6) Name of the bank and branch that must pay. It is important to note that to be valid, checks must not contain deletions or amendments, since if any of these elements exist, the document would be invalid.

Types of checks

It should be noted that within the financial market there are several check models which will depend on the actors involved in the negotiation and the payment process for the commercial operation, then we will proceed to develop the three main types of checks that we can find within of an international negotiation.

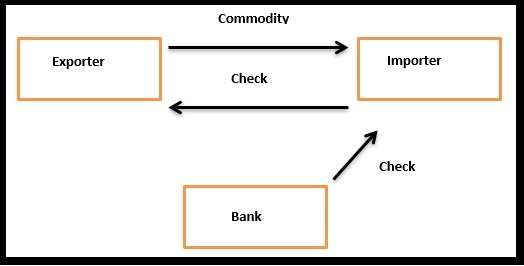

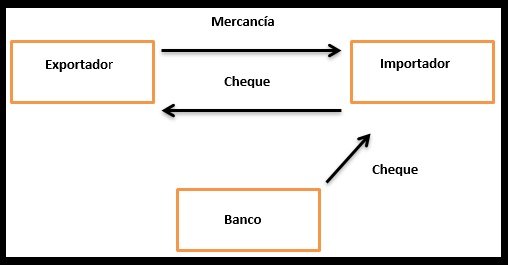

A) Bank: This payment instrument is issued by a bank related to the importer, once the exporter sends the merchandise and it is received by the importer, he orders the bank to release the corresponding payment to an account of the exporter in their respective countries.

B) Personal: This instrument can be issued by both a natural person and a legal entity, through which the exporter sends the merchandise with the respective bill of lading to the importer and once received, the latter sends the check to the exporter which can be charged to the bearer or under a specific legal or natural name.

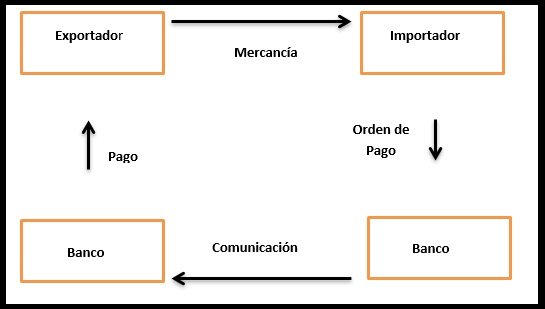

2- Bank Transfers (International Payment Order)

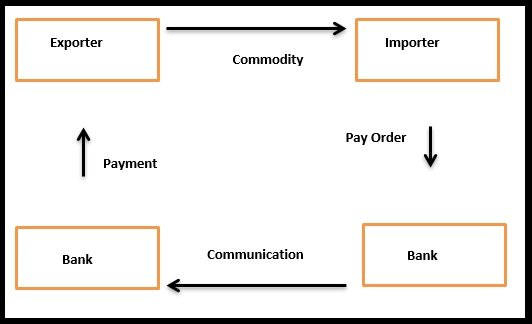

Bank transfers or international payment orders consist of sending funds from the importer to the exporter, using for this purpose firstly an issuing bank which contacts a beneficiary bank and once this relationship is established, the amount of money corresponding to the buying-selling process. It is important to highlight that this operation is completely independent of the purchase-sale contract, since at the time of payment the importer must have the necessary money in his account to order the transaction, which is discounted immediately.

Although at first glance it seems that international transfers are very simple mechanisms, we can classify them into different types depending on their nature:

A) O.P. Simple: It is the transfer of funds easily collectible by the beneficiary with the simple presentation of a bank receipt.

B) O.P. Conditional: Payment collection is subject to compliance with a prior condition or requirement. (delivery or review of some document)

C) O.P. Documentary: The payment is released once the documents proving the shipment of the merchandise are recorded.

D) O.P. Non-transferable: It can only be collected by the beneficiary, since according to international standards and in order to avoid money laundering, any payment order can only be collected by the beneficiary.

E) O.P. Transferable: It is the one that can be collected by a second beneficiary to whom the first beneficiary transfers the rights. To be transferable, the O.P. You must expressly state it.

F) O.P. Revocable: The Payment Order can be revoked at any time without prior notice or consent of the beneficiary unless it is executed or the collection process has started.

G) O.P. Irrevocable: It is one that cannot be revoked without the direct consent of the beneficiary.

H) O.P. Indivisible: Payment must be made in full and at one time.

I) O.P. Divisible: Payment may be collected in fractional forms.

J) O.P. Advance: Payment can be made even if the merchandise has not yet been shipped.

K) O.P. Deferred: Corresponds to the payment of an export that is made once the shipment was made previously.

L) O.P. Postal: Payment is sent by mail, air or sea. (Currently this method is no longer used).

M) O.P. Telegrafica: Payment is issued by cable.

N) O.P. Swft: Payment is issued via satellite, to which not all banks are necessarily associated.

Once the destination bank receives the resources, it is obliged to notify the beneficiary that his payment has been made and if there is a process where he must present some documentation, the bank agent is obliged to communicate said requirement, normally the Banks await the response and the corresponding documentation within a period of up to 180 days and if a favorable response is not received then the financial institution could return the money to its original account.

International transfers are usually a fast and secure instrument for the payment of goods and services, it also allows a wide variety of mechanisms that can be adjusted to the specific needs of each commercial operation and distances are not an impediment for the execution of said operations. , since these processes are currently highly computerized.

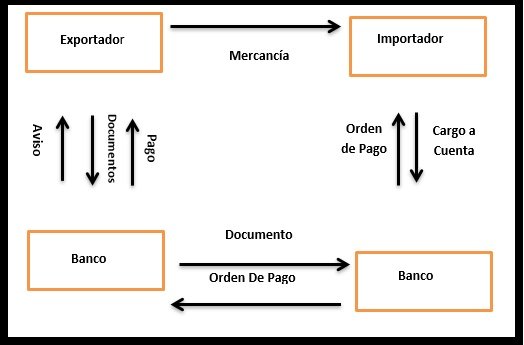

3- Documentary Collection:

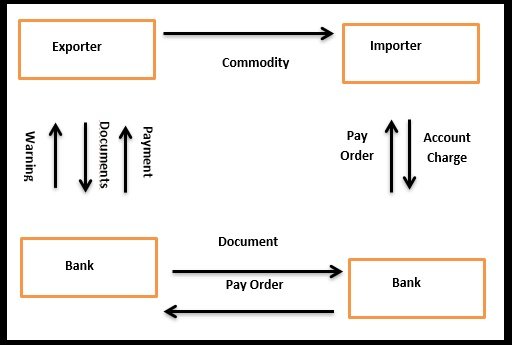

Documentary collection refers to the order that the importer sends to his bank to pay the exporter the corresponding amount of money, with the condition that the latter submit to the bank a series of documents that the importer previously requests. , payment orders do not have their own legislation and do not have the principle of irrevocability.

In this commercial operation, the bank acts as simple mediators, therefore they do not have any kind of responsibility for the money that is being traded. To understand more clearly the operation of documentary collections, it is vitally important to classify them as follows:

According to its nature

A) Simple Collection: It consists of the individual collection of values by the beneficiary without the prior consignment of the shipping documents of the merchandise.

B) Documentary Collection: It consists of the collection of the payment through the previous consignment of the shipping documents or through the acceptance of the payment in installments.

According to your payment method

A) Collection at Sight: It refers to the type of collection that must be paid to the beneficiary immediately, by presenting the payment receipt, bill of exchange or promissory note.

B) Term Collection: Payment must be made once a period of time has elapsed and on a previously determined date.

1) To Fixed Date: The expiration runs from a certain date, which is normally the bill of lading.

2) A Variable Date: The expiration date begins once the bill of exchange is accepted by the importer.

Depending on your security

A) Collection without Guarantee: The only person responsible is the accepting party without having any guarantee.

B) Collection with Guarantee: It is the one that, apart from having the acceptor as responsible, also has other co-obligors who ensure compliance with the stipulations, in most cases this co-responsibility is usually taken by the bank.

C) Collection without Pledge: In this there is no pledge as a guarantee of payment.

D) Collection with Pledge: Apart from having the acceptor's responsibility, a pledge is placed on the transaction as a guarantee of compliance, this is often widely used when capital goods are being traded.

Based on your legal resources

A) Collection without protest: In this type of collection, no legal protest is made at the time of non-payment or non-acceptance

B) Collection with Protest: When there is a lack of payment or acceptance, a legal protest can be made, which should be established in one of the collection clauses and from the moment of non-compliance it counts with a period of 48 hours to execute said legal action.

It can be seen how international documentary collection is an instrument that allows the payment of goods and services acquired in a fairly secure way, although it does not have the speed of other mechanisms, therefore it is an option to consider according to the requirements of each process. buy and sell

4- International Letter of Credit

This means of payment arises from the need to provide the commercial operation with greater security and speed of collection by the beneficiary, this instrument is usually used when there is no trust between the participants in the commercial business, therefore, for its operation, a banking entity, which serves as issuer, always acting at the request of the importer and this institution will be in charge of making the corresponding payment to the exporter, this always when the condition of presenting the corresponding necessary documentation is met, which in most cases has to be Regarding the shipment, it is important to highlight that these must comply with the parameters established in the documentary credit.

To understand a little more how this payment instrument works, it is important to make the following classification:

A) Simple or free credit: The payment can be collected only with the presentation of a simple receipt.

B) Documented Credit: Payment is made only once the shipping documents for the merchandise are presented.

C) Combined Credit: An advance payment is made to the importer before shipping the merchandise and the other part is paid once the shipping documents are presented.

D) Commercial Credit: It is the one that the issuing bank opens to the beneficiary without the participation of the importer's bank.

E) Credit Credit: Corresponds to the credit that the issuing bank opens with the intervention of a bank on the importer's beach, which is the one that gives the corresponding notice.

F) Subsidiary Credit: It is the credit reopened by the correspondent bank by order of the issuing bank and can be canceled in the name of a new beneficiary.

G) Stand By Credit: These are the guarantees by the issuing bank in favor of a beneficiary, this may or may not be due to a commercial type operation.

H) Irrevocable Credit: It cannot be revoked under any circumstances and at any stage of the business relationship.

I) Revocable Credit: It can be revoked at any instance of the commercial operation without the need to consult with the beneficiary.

J) Confirmed Credit: The exporter's bank adds a payment guarantee in the name of the banking institution, which provides greater security and confidence in the commercial operation.

K) Unconfirmed Credit: The exporter's bank does not take any responsibility regarding payment, it is important to note that all credits are unconfirmed unless they have a clause that expresses otherwise.

L) Transferable Credit: It can be transferred to a second beneficiary but only on a single occasion.

M) Non-transferable Credit: It cannot be transferred to a second beneficiary.

N) Revolving Credit: It is the one that once it is collected, it re-enters into force for the same initial amount, this many times is stipulated by the parties.

O) Divisible Credits: Are those that can be partially collected and therefore allows the exporter to partially ship the merchandise.

P) Indivisible credits: This means requires the shipment of the entire merchandise in order to be charged the same for the entire amount.

Q) Restricted Credit: It is one that can only be used or charged at the bank that is expressed by the issuing bank.

R) Unrestricted Credit: It can be charged at any bank.

S) Demand Credit: Must be paid instantly and in cash.

T) Deferred Payment Credit: This is payable at a certain time, normally after the date of shipment.

U) Acceptance Credit: It is the one that is collected when the credit has acceptance of a bill of exchange issued by the beneficiary and that must be drawn against the issuing bank

V) Financing Credit: Corresponds to the credit that is collected by the beneficiary in whole or in part before the moment of shipment of the merchandise.

1) Red Clause: Payable against simple receipt and the beneficiary agrees to ship the merchandise and otherwise must refund the amount collected.

2) Green Clause: Payable against simple receipt and the beneficiary agrees to ship the merchandise and otherwise must refund the amount collected, but also a pledge is added as a guarantee.

It can be determined that international credits enjoy greater guarantees and better security components, therefore currently they are widely used to avoid scams or legal inconveniences at the level of international trade, in addition, as described, this is the instrument that most It is used among merchants who have little confidence in each other or who are just beginning an active commercial relationship. In addition, small and new exporters also tend to use this tool, which shields commercial operations, guaranteeing that the financial transaction is transparent and secure.

Conclusion

Activities related to import and export business processes handle large amounts of money, therefore these operations must be protected by efficient means of payment that allow transparent and secure transactions, in order to avoid the possibility of criminal offenses. by law, such as fraud, insolvency or money laundering. That is why, over time, payment mechanisms have been developed that have motorized world trade and allow the participation of all actors without discriminating by size, experience or economic capabilities.

It is important to highlight how these instruments are so broad that it is possible to go from a bilateral or personal negotiation when there is a high degree of reliability between the parties through the use of personal or bank checks, to the possibility of trading goods with little-known exporters and, therefore, both with low reliability through the use of any type of international credit supported or not.

It is also necessary to highlight that in most cases, for the importer to be able to collect the merchandise sold, he must submit to the bank the respective shipping documents for the exported merchandise, which could be considered as a guarantee of That the acquired goods have already been dispatched effectively and safely and therefore payment can be released, this can be clearly seen through the use of instruments such as documented collection.

Through the use of new technologies and in order to expedite commercial and financial transactions, payments can be made through international transfers, in which the money would be transferred directly from one account to another enjoying the respective security guarantees, at You can also apply the personal transaction or through bank management with the guarantee of the presentation of the corresponding documentation.

.

The means of payment in foreign trade are without a doubt the real way to carry out commercial operations and achieve a benefit for both the exporter and the exporter, and as it has been possible to demonstrate in these transactions, natural or legal persons can participate regardless of their size, level of trust or the existing distance between both actors.

Bibliographic References

Ministry of Foreign Trade and Tourism. (2006). Forms and Means of International Payments

Practical Guide to Foreign Trade

Means of Payment and International Documentation

Modalities of Collection and Payment in International Trade

Versión en Español

Medios e Instrumentos de Pago En el Comercio Internacional

Introducción

Para el buen desarrollo de todas las operaciones relacionadas con el comercio exterior es un factor fundamental determinar y esclarecer lo relacionado al pago de los bienes o servicios adquiridos, ya que en la mayoría de los casos cuando nos adentramos en los procesos de importación y exportación esto se traduce en grades sumas de dinero que se encuentran en juego.

En estos procesos comerciales existen básicamente tres actores fundamentales, en primer lugar se tiene al importador, el cual no es más que la persona sea natural o jurídica que realiza la compra y por lo tanto es la responsable de realizar el correspondiente pago, en segundo lugar tenemos al exportador, el cual igualmente puede ser una persona natural o jurídica, pero en esta oportunidad este es el encargado de realizar el despacho del bien o servicio que se está transando y por ende este último se convierte en el beneficiario del respectivo pago y por último se tiene al banco, el cual siempre servirá de factor de conexión entre el importador, esta entidad suele tener diversos roles dependiendo del proceso de la transacción financiera, es decir en algunos casos puede ser un simple mediador mientras que en otros es un garante indiscutible de pago.

En la presente investigación de carácter descriptiva se hace referencia a los diversos medios de pago que existen dentro del comercio exterior, por lo tanto se realiza una respectiva conceptualización de cada uno de ellos y se precede a clasificarlos según sus características, con lo cual se busca alcanzar una mayor comprensión de los mismos y poder determinar en qué circunstancias son usados, además en esta clasificación también se realizan diversas valoraciones que van desde la confianza existentes entre las partes hasta los factores de seguridad que resultan determinantes para la concreción de la compra.

A modo de simplificación y para lograr una mayor comprensión del trabajo realizado como punto final de esta investigación se presenta un esquema que desglosa de forma didáctica y sencilla todos los medios de pago y sus clasificaciones existentes dentro del comercio internacional tal y como lo conocemos en la actualidad.

Para concretar una operación comercial a nivel de exportación e importación, es importante conocer los diversos medios de pago existentes en el comercio internacional, ya que es a través de instrumentos financieros mediante los cuales se poder realizar la cancelación dineraria correspondiente al costo de los bienes y servicios que son transados, es importante resaltar que estos instrumentos cuentan con altos estándares d seguridad y transparencia, además su versatilidad permite adoptarse a las circunstancias propias de cada operación comercial.

Factores que determinaran la elección en el medio de pago

Así como sucede en cualquier operación comercial cuando hablamos de pagos en los procesos de exportación e importación es importante destacar que la elección de instrumento de cancelación dependerá de diversos factores que serán determinados entre comprador y vendedor. En el comercio internacional no existe un manual o una regla que determine con exactitud que instrumento se debe utilizar, por lo tanto esto es considerado un asunto que en la cotidianidad se resuelve directamente en los procesos de negociación directa que se dan entre las partes involucradas, las cuales de modo general y más común se puede determinar que los factores determinantes en la mayor de los casos son los siguientes:

A) Grado de confianza existente entre las partes: Este factor es determinante en la relación comercial, ya que al existir mayor confianza se podrían escoger medios de pago más flexibles o abiertos, mediante los cuales la operación financiera resultaría más rápida.

B) Costos: El precio de la mercancía transada también determinara la mejor forma de pago de la misma.

C) Tamaño de las Partes: La capacidad económica tanto del comprador como del vendedor determinaran las formas de pago que pueden ser de contado o mediante créditos bancarios.

D) Riesgo País: Algunos autores incluyen al riesgo país dentro de los factores determinantes en la elección del medio de pago, ya que cuando hablamos de un Estados que se encuentra convulsionado o inmerso en circunstancias económicas desfavorables no será lo más recomendable aceptar pagos provenientes de créditos bancarios o métodos similares, sino al contrario los métodos que son directos y al contado son los preferidos para así evitar una posible insolvencia.

Mediante esta descripción se puede observar que los factores que intervienen en la elección del medio de pago son muy variables y dependen exclusivamente de la relación entre comprador y vendedor, lo cual permite flexibilizar los tramites y ajustarse a las necesidades puntuales de las partes involucradas en la operación, además de que se garantiza la seguridad y confiabilidad en los pagos.

Medios de Pago en el Comercio Internacional

Se denomina como medio o instrumento de pago internacional a aquellos mecanismos o modalidades operativas mediante las cuales el importador puede cancelar el contrato o compromiso de pago contraído con el exportador como consecuencia de la compra o contratación de un bien o servicio comercial, el cual en la mayoría de los casos estará descrito en un documento legal denominado Contrato de Compra-Venta internacional. Dentro de los medios de pago podemos destacar los siguientes:

1- Cheques

Un cheque es un documento de carácter contable mediante el cual una persona es autorizada para extraer o cobrar cierta cantidad de dinero de una cuenta, la cual se encuentra depositada en una entidad bancaria sin contar con la presencia dicha del titular de dicha cuenta. Los cheques suelen ser uno de los métodos más seguros para a cancelación de bienes y servicios en el exterior, ya que es perfectamente verificable en cuanto a los fondos se refiere, además representan un documento de carácter legal el cual podrá ser usado como prueba en caso de un incumplimiento de pago.

Los cheques a nivel internacional presentan una estructura similar, mediante lo cual se busca un mayor entendimiento y mayor seguridad, los datos que deben contener dichos mecanismos de pago son los siguientes: 1) Fecha de Emisión. 2) Monto en letras y números. 3) Lugar de Pago (donde está radicada la cuenta) 4) Nombre del Beneficiario 5) Numero y nombre de la cuenta del librador. 6) Nombre del banco y sucursal que debe pagar. Es importante señalar que los cheques para ser validos no deben contener tachaduras ni enmiendas, ya que de existir alguno de estos elementos el documento seria invalido.

Tipos de cheques

Se debe señalar que dentro del mercado financiero existen varios modelos de cheque los cuales dependerán los actores que intervengan dentro de la negociación y el proceso de pago por la operación comercial, a continuación se procederá a desarrollar los tres principales tipos de cheques que podemos encontrar dentro de una negociación internacional.

A) Bancario: Este instrumento de pago es emitido por una entidad bancaria relacionada con el importador, una vez que el exportador envía la mercancía y es recibida por el importador, este ordena al banco que se libere el correspondiente pago a una cuenta del el exportador en su respectivo país.

B) Personal: Este instrumento puede ser emitido tanto por una persona natural como por una persona jurídica, mediante el cual el exportador envía la mercancía con la respectiva nota de embarque al importador y una vez recibida este último le envía el cheque al exportador el cual puede ser cobrado al portador o bajo un nombre jurídico o natural en específico.

2- Transferencias Bancarias (Orden de pago Internacional)

Las trasferencias bancarias u órdenes de pago internacional consisten en el envío de fondos desde el importador al exportador sirviéndose para tal fin en primer lugar un banco emisor el cual se contacta con un banco beneficiario y una vez establecida esta relación se transfiere la cantidad dineraria correspondiente al proceso de compra – venta. Es importante resaltar que esta operación es totalmente independiente al contrato de compra – venta, ya que al momento del pago el importador debe contar con el dinero necesario en su cuenta para ordenar la transacción, la cual es descontada de forma inmediata.

Aunque a simple vista pareciera que las transferencias internacionales so mecanismos muy sencillos, estas las podemos clasificar en diversos tipos según sea su naturaleza:

A) O.P. Simple: Es la trasferencia de fondos fácilmente cobrables por el beneficiario con la simple presentación de un recibo bancario.

B) O.P. Condicionada: El cobro del pago queda sujeto al cumplimiento de una condición o exigencia previa. (la entrega o revisión de algún documento)

C) O.P. Documentaria: El pago se libera una vez que se consignes los documentos probatorios del embarque de la mercancía.

D) O.P. Intransferible: Solo puede ser cobrada por el beneficiario, ya que según normas internacionales y con la finalidad de evitar el lavado de dinero, toda orden de pago solo puede ser cobrada por el beneficiario.

E) O.P. Transferible: Es la que puede ser cobrada por un segundo beneficiario al que el primer beneficiario transfiere los derechos. Para ser transferible, la O.P. debe establecerlo expresamente.

F) O.P. Revocable: La Orden de pago puede ser revocada en cualquier momento sin previo aviso o consentimiento del beneficiario a menos que esta se encuentre ejecutada o se haya iniciado el proceso de cobro.

G) O.P. Irrevocable: Es aquella que no puede ser revocada sin el consentimiento directo del beneficiario.

H) O.P. Indivisible: El pago debe ser efectuado de forma íntegra y en un solo momento.

I) O.P. Divisible: El pago puede ser cobrado en formas fraccionadas.

J) O.P. Anticipada: El pago se puede realizar así aún no se haya embarcado la mercancía.

K) O.P. Diferida: Corresponde al pago de una exportación que se realiza una vez que el embarque fue realizado con anterioridad.

L) O.P. Postal: El envío del pago se realiza mediante correo, vía aérea o marítima. (En la actualidad ya este método no es usado).

M) O.P. Telegrafica: El pago es emitido por cable.

N) O.P. Swft: El pago es emitido de forma satelital, a la cual no necesariamente están asociados todos los bancos.

Una vez que el banco de destino recibe los recursos este se encuentra en la obligación de avisarle al beneficiario que su pago fue realizado y de existir algún proceso donde este deba presentar alguna documentación el agente bancario está en la obligación de comunicar dicho requerimiento, normalmente los bancos esperan la respuesta y la documentación correspondiente en un lapso de hasta 180 días y de no recibiera una respuesta favorable entonces la entidad financiera podría devolver el dinero a su cuenta de origen.

Las transferencias internacionales suelen ser un instrumento rápido y seguro para el pago de bienes y servicios, además permite una gran variedad de mecanismos que se pueden ajustar a las necesidades puntuales de cada operación comercial y las distancias no son un impedimento para la ejecución de dichas operaciones, ya que en la actualidad estos procesos se encuentran altamente computarizados.

3- Cobranza Documentaria:

La cobranza documentaria hace referencia a la orden que el importador le gira a su banco para que le cancele al exportador la cantidad correspondiente de dinero, con la condición de que este último presente ante la entidad bancaria una serie de documentos que el importador solicita con anterioridad, las órdenes de pago no poseen una legislación propia y no cuentan con el principio de irrevocabilidad.

En esta operación comercial el banco actúan como simples mediadores, por lo tanto no poseen ninguna clase de responsabilidad por el dinero que se está transando. Para entender con mayor claridad el funcionamiento de las cobranzas documentales en de vital importancia clasificarlas de la siguiente manera:

Según su naturaleza

A) Cobranza Simple: Consiste en el cobro individual de valores por parte del beneficiario sin la previa consignación de los documentos de embarque de la mercancía.

B) Cobranza Documentaria: Consiste en el cobro del pago mediante la previa consignación de los documentos de embarque o mediante la aceptación del pago en plazos.

Según su forma de pago

A) Cobranza a la Vista: Hace referencia al tipo de cobranza que debe ser cancelada al beneficiario de forma inmediata, mediante la presentación del recibo de pago, letra de cambio o pagare.

B) Cobranza a Plazo: El pago debe ser realizado en una vez ha trascurrido un lapso de tiempo y en fecha previamente determinada.

1) A Fecha Fija: El vencimiento corre a partir de cierta fecha, la cual normalmente es la del conocimiento del embarque.

2) A Fecha Variable: El vencimiento comienza a correr una vez la letra de cambio sea aceptada por el importador.

En función de su seguridad

A) Cobranza sin Aval: El único responsable es la parte aceptante sin contar con ninguna garantía.

B) Cobranza con Aval: Es la que aparte de tener como responsable al aceptante, también cuenta con otros coobligados que velan por el cumplimiento de lo estipulado, en la mayoría de los casos esta corresponsabilidad suele tomarla el banco.

C) Cobranza sin Prenda: En esta no está presente ninguna prenda como garantía de pago.

D) Cobranza con Prenda: Aparte de contar con la responsabilidad dl aceptante, se le coloca a la transacción un prenda en garantía de su cumplimiento, esto suele ser muy usado cuando se están transando bienes de capital.

En función de sus recursos legales

A) Cobranza sin protesto: En este tipo de cobranza no se realiza ningún protesto legal al momento de existir un incumplimiento de pago o falta de aceptación

B) Cobranza con Protesto: Al momento de que existiese una falta de pago o aceptación se puede proceder a un protesto legal, el cual debería estar establecido en una de las cláusulas de la cobranza y a partir del momento del incumplimiento se cuenta con un lapso de 48 horas para ejecutar dicha acción legal.

Se puede apreciar como la cobranza documentaria internacional es un instrumento que permite el pago de los bienes y servicios adquiridos de forma bastante segura aunque no cuenta con la velocidad de otros mecanismos, por lo tanto es una opción a considerar según los requerimientos de cada proceso de compra- venta

4- Carta de Crédito Internacional

Este medio de pago surge de la necesidad de brindarle a la operación comercial de mayor seguridad y rapidez de cobro por parte del beneficiario, esta instrumento suele ser usado cuando no existe confianza entre los intervinientes del negocio comercial, por lo tanto para su funcionamiento interviene una entidad bancaria, que sirve como emisor obrando siempre a petición del importador y esta institución será la encargada de realizar el correspondiente pago al exportador, esto siempre cuando se cumpla la condición d presentar la correspondiente documentación necesaria, que en la mayoría de los casa tiene que ver con lo relativo al embarque, es importante resaltar que estos deben cumplir con los parámetros establecidos en el crédito documentario.

Para entender un poco más como es el funcionamiento de este instrumento de pago es importante realizar la siguiente clasificación:

A) Crédito Simple o libre: El pago puede ser cobrado solo con la presentación de un recibo simple.

B) Crédito Documentado: El pago es realizado solo una vez que se presenten los documentos de embarque de la mercancía.

C) Crédito Combinado: Se realiza un pago anticipado al importador antes de enviar la mercancía y la otra parte se cancela una vez se presenten los documentos de embarque.

D) Crédito Comercial: Es el que abre el banco emisor al beneficiario sin la participación del banco del importador.

E) Crédito Acreditivo: Corresponde al crédito que abre el banco emisor con la intervención de un banco en la playa del importador, el cual es el que da el aviso correspondiente.

F) Crédito Subsidiario: Es el crédito reabierto por el banco corresponsal por orden del banco emisor y puede ser cancelado a nombre de un nuevo beneficiario.

G) Stand By Credit: Se trata de las garantías por el banco emisor a favor de un beneficiario, esto pudiera obedecer o no a una operación del tipo comercial.

H) Crédito Irrevocable: No puede ser revocado bajo ninguna circunstancia y en ninguna etapa de la relación comercial.

I) Crédito Revocable: Puede ser revocado en cualquier instancia de la operación comercial sin necesidad de consultar con el beneficiario.

J) Crédito Confirmado: El banco del exportador agrega una garantía de pago a nombre de la institución bancaria, con lo cual se brinda mayor seguridad y confianza en la operación comercial.

K) Crédito No Confirmado: El banco del exportado no toma ninguna responsabilidad en cuanto al pago, es importante resaltar que todos los créditos son no confirmados a menos que posee una cláusula que exprese lo contrario.

L) Crédito Transferible: Puede ser transferido a un segundo beneficiario pero solo en una sola ocacion.

M) Crédito Intransferible: El mismo no puede ser transferido a un segundo beneficiario.

N) Revolving Credit: Es aquel que una vez sea cobrado vuelve a entrar en vigor por la misma cantidad inicial, esto tantas veces este estipulado por las partes.

O) Créditos Divisibles: Son aquellos que pueden ser cobrados en forma parcial y por lo tanto le permite al exportador embarcar la mercancía de forma parcial.

P) Créditos indivisibles: Este medio exige el embarque de la totalidad de la mercancía para poder ser cobrado igual en la totalidad del importe.

Q) Crédito Restringido: Es aquel que solo puede ser usado o cobrado en la entidad bancaria que sea expresada por el banco emisor.

R) Crédito No Restringido: Puede ser cobrado ante cualquier entidad bancaria.

S) Crédito A la Vista: Debe ser cancelado al instante y al contado.

T) Crédito De pago Diferido: Este es pagadero en un tiempo determinado, normalmente después de que se dé la fecha de embarque.

U) Crédito de Aceptación: Es aquel que cobrado cuando el crédito dispone aceptación de letra de cambio librada por el beneficiario y que deben ser giradas contra el banco emisor

V) Crédito de Financiamiento: Corresponde al crédito que es cobrado por el beneficiario de forma total o parcial antes del momento del embarque de la mercancía.

1) Clausula Roja: Pagadero contra simple recibo y el beneficiario se compromete a embarcar la mercancía y de lo contrario debe reintegrar el importe cobrado.

2) Clausula Verde: Pagadero contra simple recibo y el beneficiario se compromete a embarcar la mercancía y de lo contrario debe reintegrar el importe cobrado, pero además se le agrega una prenda en condición de garantía.

Se puede determinar que los créditos internacionales gozan con unas mayores garantías y mejores componentes de seguridad, por lo tanto en la actualidad son ampliamente usados para evitar estafas o inconvenientes legales a nivel del comercio internacional, además como se ha descrito este es el instrumento que más se usa entre comerciantes que se tienen poca confianza o que apenas están iniciando una relación comercial activa, además los pequeños y nuevos exportadores también suelen hacer uso de esta herramienta lo cual blinda las operaciones comerciales garantizando que la transacción financiera se trasparente y segura.

Conclusión

Las actividades relacionadas con los procesos comerciales de importación y exportación manejan grandes cantidades de dinero, por lo tanto estas operaciones deben ser resguardadas por medios de pago eficientes que permitan transacciones trasparentes y seguras, para de este modo evitar la posibilidad de la formación de delitos penados por la ley, tales como estafas, insolvencias o lavado de capitales. Es por ello que a lo largo del tiempo se han desarrollado mecanismos de pago que han motorizado al comercio mundial y permiten la participación de todos los actores sin discriminar por tamaño, experiencia o capacidades económicas.

Es importante resaltar como estos instrumentos resultan tan amplios que se pude pasar de una negociación bilateral o personal cuando existe alto grado de confiabilidad entre las partes mediante el uso de cheques personales o bancarios, hasta la posibilidad de transar bienes con exportadores poco conocidos y por lo tanto con una baja confiabilidad mediante el uso de cualquier tipo de crédito internacional respaldado o no.

También es necesario resaltar que en la mayoría de los casos para que el importador pueda realizar el cobro de la mercancía vendida este debe presentar ante el banco los respectivos documentos de embarque de la mercancía exportada, con lo cual se podría considerar que es una garantía de que los bienes adquiridos ya fueron despachados de forma efectiva y segura y por lo tanto se puede liberar el pago, esto se puede apreciar con claridad mediante el uso de instrumentos como la cobranza documentada.

Mediante el uso de las nuevas tecnologías y con la finalidad de agilizar las transacciones comerciales y financieras, los pagos pueden ser realizados mediante transferencias internacionales, en las cuales el dinero se trasladaría directamente de una cuenta a otra gozando de las respectivas garantías de seguridad, al igual puede aplicar la transacción personal o mediante la gestión bancaria con el aval de la presentación de la documentación correspondiente.

.

Los medios de pago en el comercio exterior son sin duda alguna la forma real de concretar las operaciones comerciales y lograr un beneficio tanto para el exportador como para el exportador y como se ha podido demostrar en estas transacciones pueden participar personas naturales o jurídicas sin importar su tamaño, nivel de confianza o la distancia existente entre ambos actores.

Referencias Bibliográficas

Ministerio de Comercio Exterior y Turismo. (2006). Formas y Medios de Pagos Internacionales

Guía Práctica de Comercio Exterior