03-05-2024 - Economy - Reclassification of the Income Statement [EN]-[IT]

~~~ La versione in italiano inizia subito dopo la versione in inglese ~~~

ENGLISH

03-05-2024 - Economy - Reclassification of the Income Statement [EN]-[IT]

Reclassification of the Income Statement

Note

Financial statement reclassification is an activity that is carried out to ensure that the financial statement takes on a more readable form. In this form you don't have to be an accountant to understand a balance sheet.

The balance sheet is made up of 3 main sections, the Balance Sheet, the Income Statement and the Explanatory Notes.

Regarding the reclassification of the Income Statement we must know that there are three methods or three models:

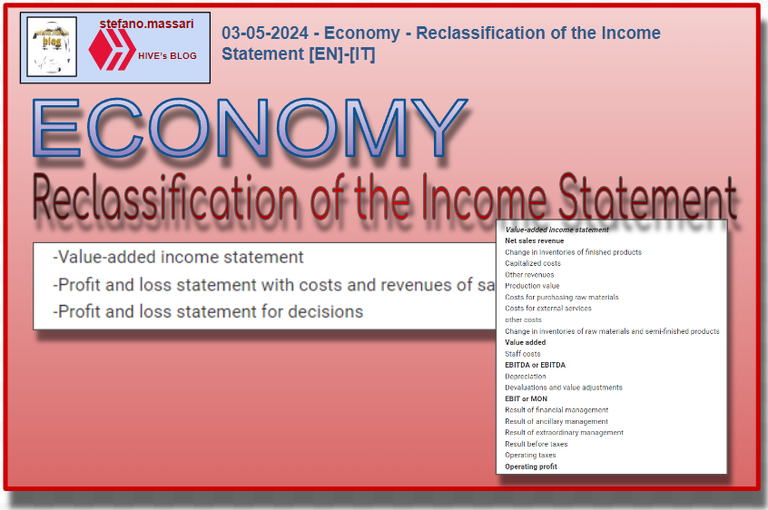

-Value-added income statement

-Profit and loss statement with costs and revenues of sales

-Profit and loss statement for decisions

Value-added income statement

This typology contains the following indications.

Added Value measures the increase in value generated by management after deducting only the costs for raw materials and services, i.e. external costs),

The Gross Operating Margin (GOM) measures the income net of the typical operating costs and which have generated cash outflows. The Gross Operating Margin is also called Earnings Before Interest, Tax, Depreciation and Admortization (EBITDA),

The Net Operating Margin takes into account both depreciation and write-downs and therefore measures the company's earning capacity. The Net Operating Margin (MON) or Earnings Before Interest and Tax (EBIT).

NOTE: EBITDA measures operating cash flows.

Below is the list of items in a value-added income statement.

Value-added income statement

Net sales revenue

Change in inventories of finished products

Capitalized costs

Other revenues

Production value

Costs for purchasing raw materials

Costs for external services

other costs

Change in inventories of raw materials and semi-finished products

Value added

Staff costs

EBITDA or EBITDA

Depreciation

Devaluations and value adjustments

EBIT or MON

Result of financial management

Result of ancillary management

Result of extraordinary management

Result before taxes

Operating taxes

Operating profit

Profit and Loss Statement with Costs and Revenues of Sales

This type of income statement model refers to the various management areas.

For this model we need to take into account the following things, i.e. that it is built on the basis of:

-Definition of the management areas of the company

-Aggregation of operating costs according to a production destination criterion,

-Allocation of reclassified costs in the defined management areas

-Paying particular attention to the income area

-Industrial area, commercial area and administrative area.

Here we talk about the industrial gross margin, we understand how much the production of the product costs.

Contribution margin income statement

We can divide this type of income statement into two main topics:

-Takes into account the degree of rigidity and variability (fixed and variable costs)

- Mainly used to verify the use of resources in order to identify the break-even point.

Example

Let's go and get the budget document that we can find on the internet at the following link:

https://www.juventus.com/it/search?q=relazione+finanziaria+annuale

Let's take the official annual financial report issued on 06-30-2020 as an example

On page 49 we can see the Income Statement with the various items

Conclusions

To simplify the income statement of a financial statement, there are 3 methodologies, each with different reading characteristics.

Request

Have you already heard of Gross Operating Margin? When reading some financial statement data, had you already seen the acronym EBITDA?

![]()

ITALIAN

03-05-2024 - Economia - Riclassificazione del Conto Economico [EN]-[IT]

Riclassificazione del Conto Economico

Cenni

La riclassificazione di bilancio è un’attività che si esegue per fare in modo che il bilancio assuma una forma più leggibile. In questa forma non bisogna essere dei commercialisti per comprendere un bilancio.

Il bilancio è composto da 3 sezioni principali, lo Stato Patrimoniale, il Conto Economico, la Nota Integrativa.

Per quanto riguarda la riclassificazione del Conto Economico dobbiamo sapere che esistono tre metodi o tre modelli:

-Conto economico a valore aggiunto

-Conto economico a Costi e Ricavi del Venduto

-Conto economico per le decisioni

Conto economico a valore aggiunto

Questa tipologia contiene le seguente indicazioni.

Il Valore Aggiunto misura l’incremento di valore generato dalla gestione dedotti solo i costi per le materie prime e servizi, cioè i costi esterni),

Il Margine Operativo Lordo (MOL) misura il reddito al netto dei costi operativi caratteristici e che hanno generato uscite di cassa. Il Margine Operativo Lordo è detto anche Earnings Before Interest, Tax, Depreciation and Admortization (EBITDA),

Il Margine Operativo Netto tiene conto sia degli ammortamenti sia delle svalutazioni e quindi misura la capacità reddituale dell’impresa. Il Margine Operativo Netto (MON) o Earnings Before Interest and Tax (EBIT).

NOTA: Il MOL misura i flussi di cassa operativi.

Qui di seguito l’elenco delle voci di un conto economico a valore aggiunto.

Conto economico a valore aggiunto

Ricavi netti di vendita

Variazione di rimanenze di prodotti finiti

COsti capitalizzati

Altri ricavi

Valore della produzione

Costi per acquisto materie prime

Costi per servizi esterni

altri costi

Variazione rimanenze materie prime e semilavorati

Valore Aggiunto

Costi del personale

EBITDA o MOL

Ammortamenti

Svalutazioni e rettifiche di valore

EBIT o MON

Risultato della gestione finanziaria

Risultato della gestione accessoria

Risultato della gestione straordinaria

Risultato al lordo delle imposte

Imposte d’esercizio

Utile di esercizio

Conto economico a Costi e Ricavi del Venduto

Questa tipologia di modello di conto economico è riferito alle varie aree gestionali.

Per questo modello dobbiamo tenere conto delle seguenti cose, cioè che è costruito sulla base di:

-Definizione delle aree gestionali dell’azienda

-Aggregazione dei costi operativi secondo un criterio di destinazione produttiva,

-Imputazione dei costi riclassificati nelle aree gestionali definite

-Facendo particolare attenzione all’area reddituale

-Area industriale, area commerciale e area amministrativa.

Qui si parla del margine lordo industriale, si comprende quanto costa la produzione del prodotto.

Conto economico a margine di contribuzione

Questa tipologia di conto economico possiamo dividerla in due grossi argomenti:

-Tiene conto del grado di rigidità variabilità (costi fissi e variabili)

-Usato soprattutto per verificare l’utilizzo delle risorse ai fini di individuare il punto di break-even.

Esempio

Andiamo a prendere il documento di bilancio che possiamo trovare in internet al seguente link:

https://www.juventus.com/it/search?q=relazione+finanziaria+annuale

Prendiamo come esempio la relazione finanziaria annuale ufficiale emessa il 30-06-2020

A pagina 49 possiamo vedere il Conto Economico con le varie voci

Conclusioni

Per semplificare il Conto Economico di un bilancio di esercizio esistono 3 metodologie, ognuna con delle caratteristiche di lettura diverse.

Domanda

Avevate già sentito parlare di Margine Operativo Lordo? Nel leggere qualche dato di bilancio avevate già visto la sigla EBITDA?

THE END

Does Gross Operating Margin mean the same as the business capital or are they different from each other

Every business must understand the golden rule of financial management and not only that should know how to regulate it effectively

https://twitter.com/lee19389/status/1786402029113315367

#hive #posh

!discovery 30

@tipu curate

Upvoted 👌 (Mana: 35/45) Liquid rewards.

This post was shared and voted inside the discord by the curators team of discovery-it

Join our Community and follow our Curation Trail

Discovery-it is also a Witness, vote for us here

Delegate to us for passive income. Check our 80% fee-back Program

Ehi, hai molta conoscenza, ti ammiro